2024 State of the Private Lending Market

Top lenders, market commentary from active lenders, metros with largest changes in activity, borrower loyalty, and more.

Executive Summary

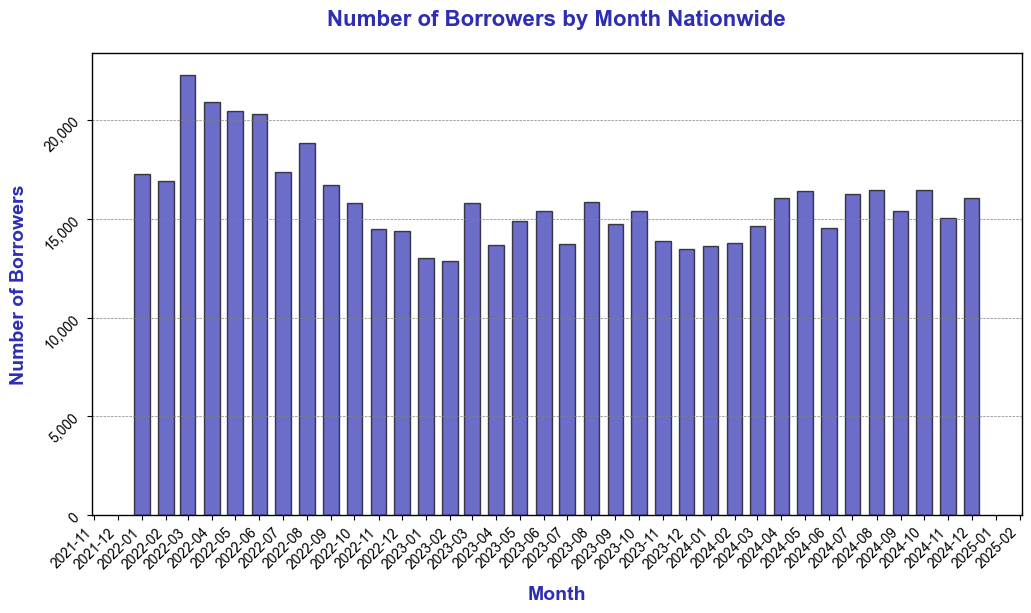

Private lending activity was up 12.3% in 2024 compared to 2023. Since reaching a low in January 2023, activity held flat to slightly positive.

Kiavi is the leading nationwide provider of fix-and-flip loans, holding the #1 market share position in 25 different markets as of December 2024.

Private lending regionally continues to be served by a long-tail of providers, with almost all regions having 50+ lenders completing 10+ loans in 2024.

At the end of the article, paid subscribers have access to a list of the top 250 borrowers by loan count - including volume and which lenders they used.

SFR Analytics Private Lender Radar

Interested in being able to track private lender activity nationwide in real-time, including getting access to borrower lists for each lender with borrower contact information? Reply to this email or reach out to support@sfranalytics.com for a demo of Private Lender Radar.

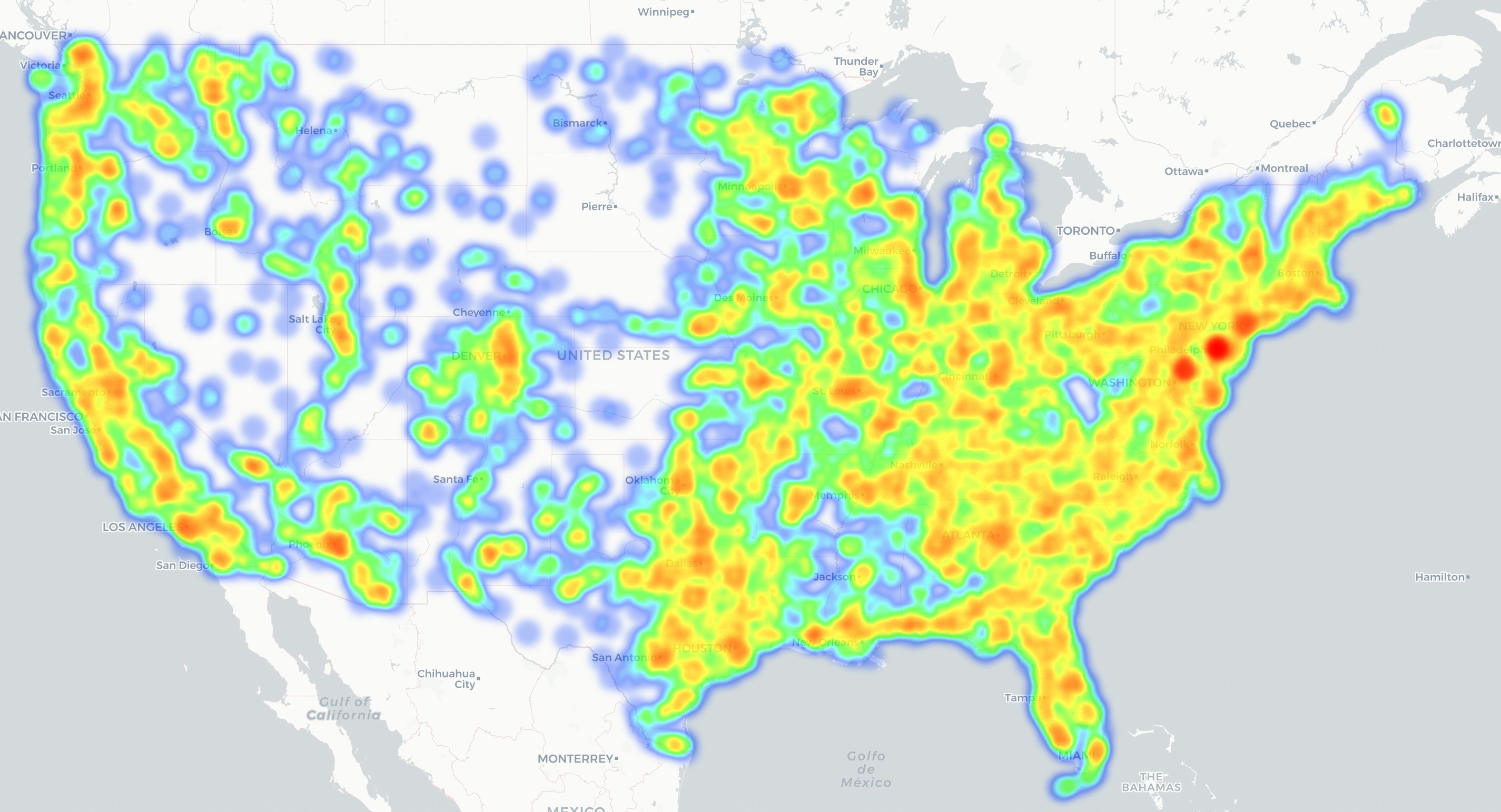

We offer nationwide coverage, supporting every metro in the US

In addition to tracking private lending activity, the tool also provides coverage of:

Cash buyers

Current holdings for an entity

Verified contact information for thousands of borrowers nationwide

Dozens of originators choose Private Lender Radar to close more deals, enter new metros successfully, and get a better real-time view of the market.

Market Commentary

SFR Analytics works with lenders nationwide; brief color shared below is based on regular conversations we have with lenders and trends we’re observing.

Competition is heating up, with lenders mentioning more borrowers are shopping deals than in the past. Lenders are spending more on marketing, hosting more happy hours, and doing more cold calls than ever before, while in some markets deals are becoming harder to pencil. This intensifies competition for each deal.

Increased competition is driving margin compression. Both origination fees and rates are decreasing.

Despite the increased competition, the majority of lenders remain optimistic about growing their business this year. Many lenders are doubling down on niches they operate well in.

Top employees are starting new lenders and former executives are getting back in the game. Last year, lenders like Ascent, Encore, and CV3 launched and quickly posted significant origination volume. Recently, top executives and reps haved started new originators. It’s getting easier to start a new lender each year and the ability to capture more of the upside can be significant.

Data Overview

At SFR Analytics, we leverage nationwide deed and assessor data to track the single family rental market. To generate this analysis, we’ve:

Identified and reconciled the entities that private lenders make loans under

Identified and reconciled the entities that investor purchase properties under

While the data used is primarily residential, some commercial originations are also included

Analysis & Results

Nationwide Activity

Private lending activity increased in 2024 compared to 2023, with steady growth continuing through the end of the year.

Average origination size held steady through most of the year.

Part of the increase in origination volume can be explained by a greater number of property investors participating, shown by the increase in the number of unique investors taking out a loan in a given month.

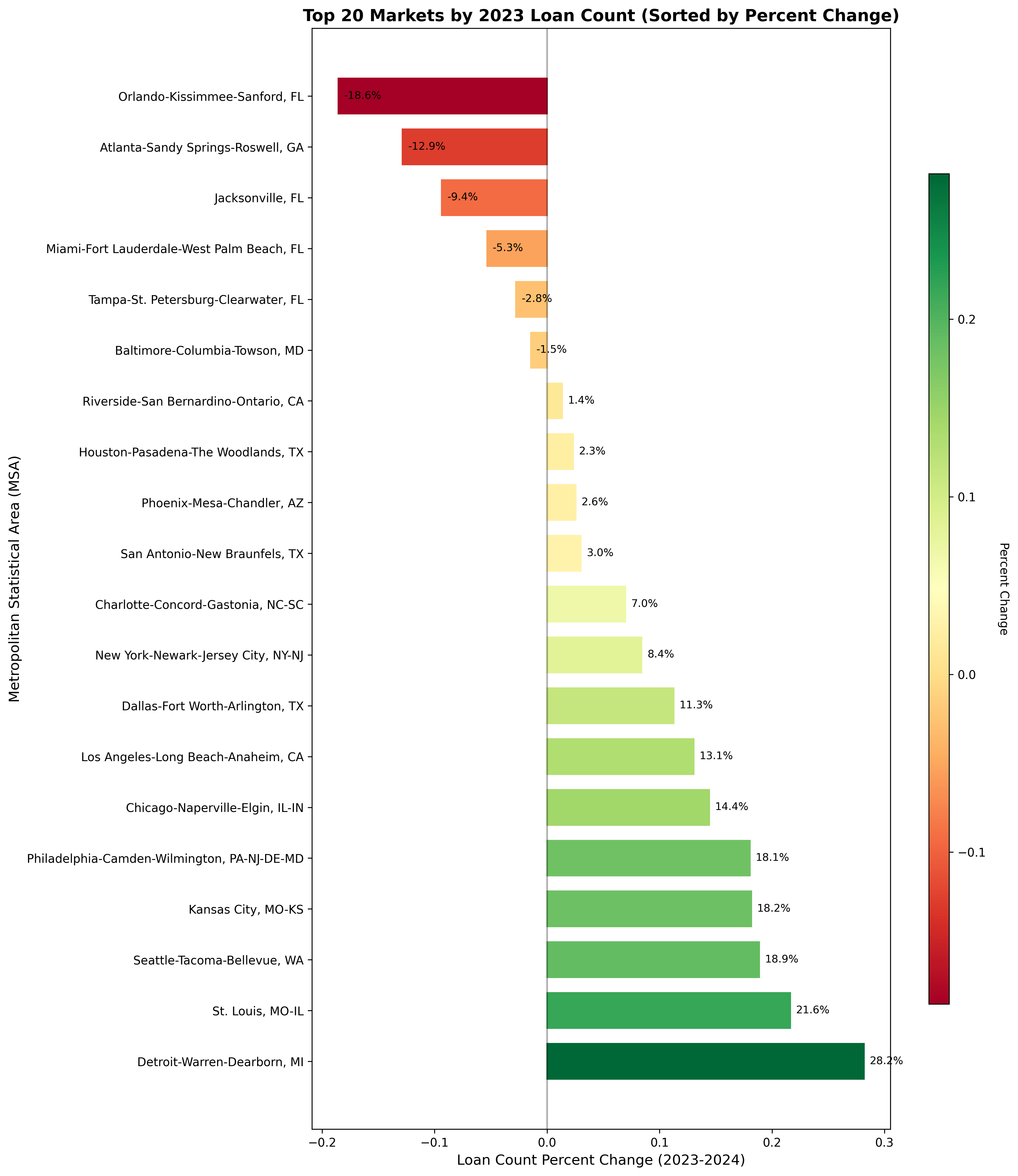

14 of The Top 20 Markets Grew In Loan Count

While Florida struggled with loan volume, the majority of other markets were flat or slightly up. Florida represented four of the six metros that had net decreases in origination activity.

Growth Consolidated With The Largest Lenders

23 of the top 25 private lenders grew year-over-year, with a median growth rate of 33%. The below graph is excludes CV3 and Encore, which are both in the top 25 but had >500% growth, which would distort the distribution of the graph.

Kiavi Market Position Over Time

Kiavi continues to be the leading nationwide private lender, ranking #1 in market share across 25 different MSAs profiled as of December 2024.

Local Dominance In Some Markets

Despite Kiavi being the largest nationwide fix-and-flip lender, there are regional lenders with top market share in a few key markets.

In 2024, Capital Fund maintained a significant presence in Phoenix, capturing nearly 14% of the market. There are many markets similar to Phoenix where regional lenders dominate.

However, regional dominance could weaken this year as nationwide companies like Renovo implement local “boots on the ground” strategies while regional lenders expand into new states.

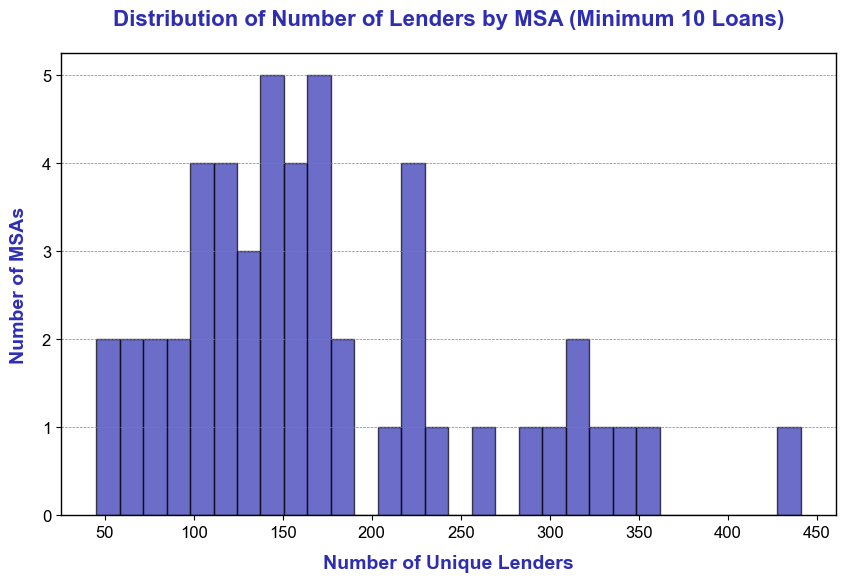

Distribution of Active Lenders by MSA

Private lending still supports a long tail of active lenders within MSAs. Most MSAs had over 100 unique lenders each completing more than 10 loans during the period from January 2024 to December 2024.

Top Borrowers

To see the top 250 borrowers last year by loan count, subscribe below

Note: the remainder of this article is available to paid subscribers, sign up below for access. Paid subscribers get full access to data-rich articles about the SFR market and select additional articles only available to paid subscribers.